SBA loans vs. business lines of credit: Which is best for small businesses?

All businesses need funds to operate, but sometimes small businesses may need a financial boost to jump-start growth or get through an off season. The U.S. Small Business Administration (SBA) helps connect small businesses to government-approved lenders who can provide support. However, not all businesses need a large loan. Some may benefit more from flexible access to credit, LegalZoom explains.

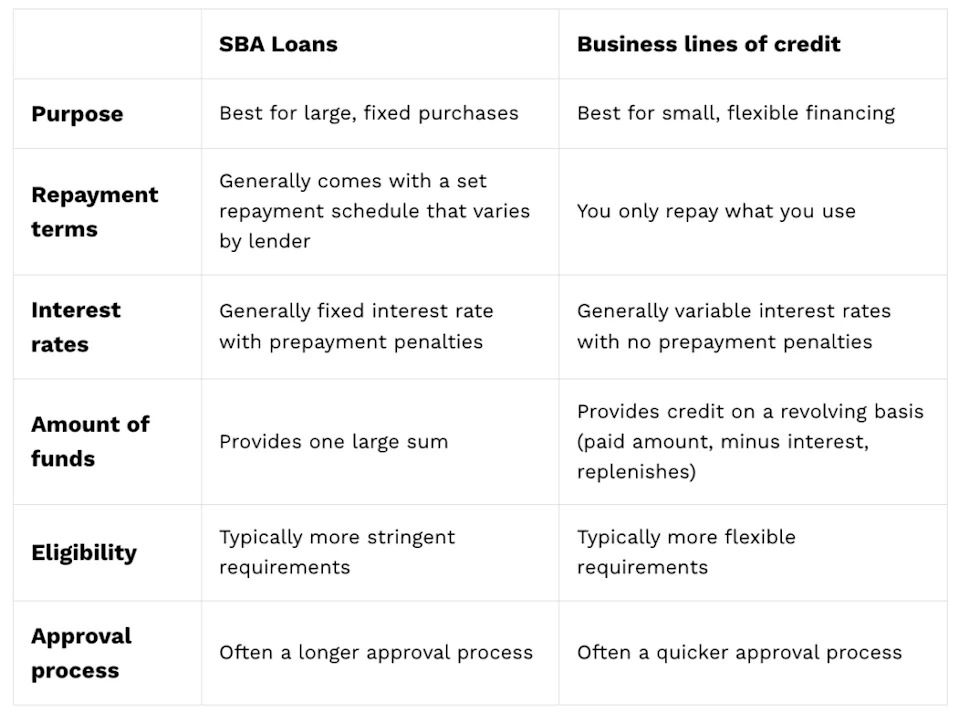

SBA loan vs. business credit line at a glance

Both an SBA-backed loan and a business credit line provide businesses with access to necessary funding. However, they differ in how they provide funds and for what purpose.

Here are some of the key differences.

What is an SBA loan?

SBA loans are government-approved loans designed to support small businesses and facilitate a safer, smoother process for both lenders and borrowers. By establishing guidelines and guarantees for business loans, SBA programs reduce lender risk and provide small businesses easier access to necessary capital.

Generally, SBA doesn't provide the loans themselves. Instead, they partner with lenders to offer a series of loan programs. Once a business chooses the right program for their financing goals, SBA matches it with a lender.

SBA does, however, directly offer low-interest loans to help businesses and homeowners recover from declared disasters .

Types of SBA loans

SBA offers four main loan programs.

Who qualifies for an SBA loan?

Generally, businesses must be creditworthy, registered for-profit organizations, based in the U.S., and meet SBA size requirements to get an SBA-backed loan. That said, each loan program has its own additional requirements.

SBA loan pros and cons

While they aren't for every business, there are many benefits to applying for an SBA-backed loan .

SBA loan pros

SBA loan cons

What is a business line of credit?

Rather than providing one large lump sum, a business line of credit allows companies to draw funds up to a predetermined limit, as needed. In this way, a business line of credit is actually more similar to a business credit card than a loan. Additionally, borrowers only need to pay interest on the amount used, not the full available sum.

Depending on the lender's policy, businesses can access these funds from a business checking account, checks, bank transfers, or cards linked to the line of credit. There are both secured and unsecured lines of credit depending on the size of the available sum. A larger sum may require you to secure the line with collateral.

A business line of credit also differs from an SBA-backed loan in that companies often use it to manage business finances rather than for one specific purpose or purchase.

Who qualifies for a business line of credit?

Requirements vary lender to lender. That said, many lenders will require businesses to have consistent revenue, strong cash flow, a detailed business plan, and a good credit score to qualify. Some lenders may also limit eligibility to businesses that have been operating for a fixed amount of time.

Business line of credit pros and cons

Like SBA loans, business lines of credit come with their own unique benefits and drawbacks that may influence whether or not the financing option is right for your business.

Line of credit pros

Line of credit cons

How to choose which financing option is right for you

When determining which financing option is right for your business, it's helpful to consider the following factors.

No matter which financing option you choose, LegalZoom can help you meet eligibility requirements and strengthen your application through various services, including patent or trademark registration.

If you still have questions about which route is best for your business, reach out to a business attorney for legal advice based on your unique circumstances.

FAQs

How long does it take to get approved for an SBA loan vs. business line of credit

The approval processing time varies by lender for both an SBA-backed loan and a business line of credit. That said, approval for an SBA loan tends to take 5-10 days just to review your application, not including the lender approval process that can take up to a month. A business line of credit can take anywhere from several days to a few weeks.

What documents do I need to apply for an SBA loan or a business line of credit?

Both financing options typically require formation documents as proof of your business’ legal structure, ownership information, your EIN , and various financial statements.

What are the interest rates for SBA loans vs. business lines of credit?

For both SBA-backed loans and business lines of credit, interest rates depend on the lender and program. The 504 loan program offers fixed-rate loans, while the 7(a) loans and microloans can be either fixed or variable. Rates generally range between 8%-13%.

Interest rates for a business line of credit range significantly by lender, depending on factors like the business owner's creditworthiness, size of the loan, and whether the interest rate is fixed or variable.

Do SBA loans have lower interest rates than business lines of credit?

While it depends on a number of factors, generally SBA-backed loans can offer lower interest rates compared to business lines of credit due to government guarantees.

This article is for informational purposes. This content is not legal advice, it is the expression of the author and has not been evaluated by LegalZoom for accuracy or changes in the law.

This story was produced by LegalZoom and reviewed and distributed by Stacker .